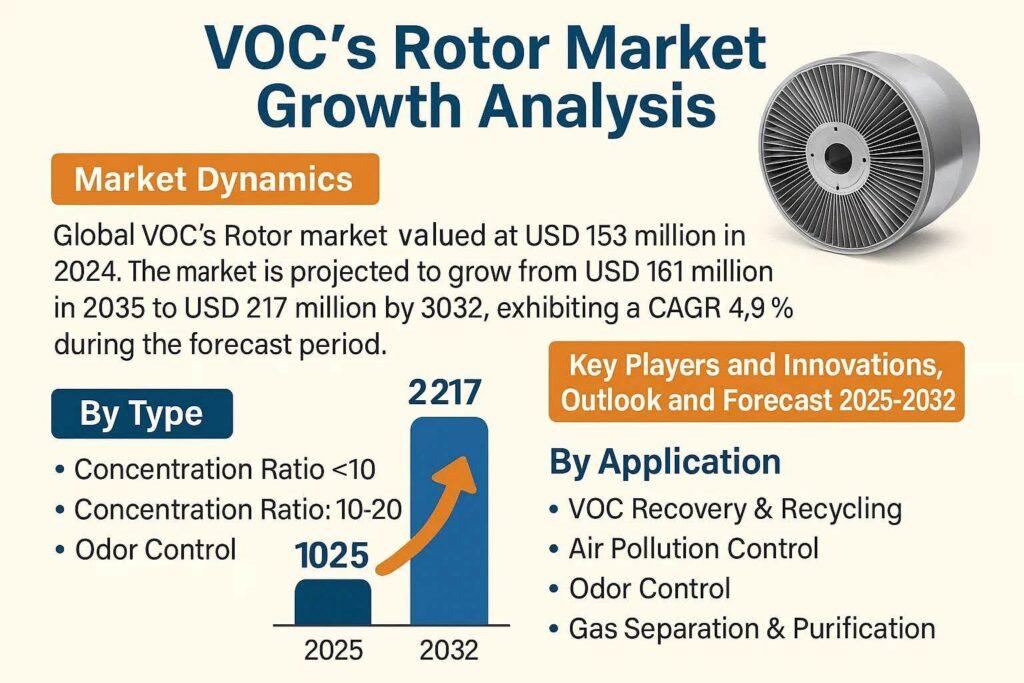

VOC’s Rotor market was valued at USD 153 million in 2024. The market is projected to grow from USD 161 million in 2025 to USD 217 million by 2032, exhibiting a CAGR of 4.9% during the forecast period.

VOC’s Rotor is an air pollution control device designed to capture and concentrate volatile organic compound (VOC) emissions for subsequent treatment or recovery. These systems play a critical role in industrial applications where emission control is mandated by environmental regulations. The technology utilizes rotating adsorption wheels with specialized media to effectively remove VOCs from exhaust streams.

What is VOC’s Rotor Technology?

VOC’s Rotor systems are continuous adsorption concentrators that capture and concentrate volatile organic compounds (VOCs) from industrial exhaust streams. These systems utilize rotating wheels coated with specialized adsorbent materials like zeolites or activated carbon to effectively remove pollutants. The technology enables 90-95% VOC removal efficiency while significantly reducing energy consumption compared to traditional thermal oxidizers. Major applications span industries including automotive, chemical processing, pharmaceuticals, and electronics manufacturing where emission control is critical.

MARKET DRIVERS

Stringent Environmental Regulations Fueling VOC Rotor Adoption

With increasing global emphasis on air pollution control and industrial emissions reduction, regulatory bodies such as the U.S. Environmental Protection Agency (EPA), European Environment Agency (EEA), and counterparts in Asia-Pacific have enforced stricter VOC (Volatile Organic Compound) emission limits. These regulations are compelling industries particularly in chemicals, paints & coatings, and electronics to adopt advanced emission control technologies. VOC rotors, with their high efficiency in concentrating and capturing VOCs from exhaust air streams, are emerging as a preferred solution. For example, the European Union’s Industrial Emissions Directive and China’s Blue Sky Protection Campaign have directly increased demand for VOC abatement systems, including rotor concentrators. As compliance becomes non-negotiable, investments in VOC control systems are surging, driving the growth of the global VOC rotor market.

Cost Efficiency Advantages Driving Market Preference

One of the primary factors accelerating the adoption of VOC rotors is their compelling cost-efficiency compared to traditional emission control technologies. VOC rotors operate by concentrating low-concentration VOC-laden air streams before directing them to thermal or catalytic oxidizers. This concentration process significantly reduces the air volume requiring treatment often by a factor of 10 or more resulting in lower energy consumption, smaller oxidizer size, and reduced fuel costs. Industries with continuous production lines, such as automotive painting, semiconductor fabrication, chemical manufacturing, and printing, benefit immensely from the operational savings. For example, in automotive paint shops where VOC emissions are high but dispersed, the use of VOC rotors has been shown to cut thermal oxidizer operating costs by up to 60% by lowering airflow to manageable levels.

Technological Advancements Expanding Application Potential

Recent technological advancements in VOC rotor systems are significantly broadening their application scope across diverse industrial sectors. Innovations in adsorbent materials, rotor design, and system integration are enhancing performance, reliability, and flexibility making VOC rotors viable for even the most demanding operational environments.

For example, the development of high-performance zeolite coatings and hybrid adsorbent materials has improved the ability of rotors to capture a wider range of VOCs, including high-boiling-point organics and halogenated compounds. Companies like Seibu Giken and Munters have introduced rotors with specialized coatings that offer superior thermal stability and chemical resistance, making them suitable for industries such as semiconductor manufacturing, pharmaceuticals, and chemical processing, where traditional systems would degrade rapidly.

MARKET OPPORTUNITIES

Asian Industrial Expansion Creating New Growth Frontiers

The rapid industrialization and urban development across Asia are opening up significant new growth opportunities for the VOC rotor market. Countries like China, India, South Korea, Vietnam, and Indonesia are witnessing a surge in manufacturing activities particularly in sectors like automotive, chemicals, electronics, textiles, and printing which are major sources of VOC emissions. This industrial boom is fueling demand for advanced air pollution control technologies that are both effective and energy-efficient.Governments in the region are also tightening environmental regulations. For example, China’s “Blue Sky” initiative and its latest VOC emission standards for key industries (GB 37822-2019) have accelerated the installation of VOC concentrator systems across chemical and coating sectors. Major electronics manufacturers in South Korea and Taiwan are integrating VOC rotors into their cleanroom ventilation systems to meet both environmental and occupational safety standards.

In India, rising awareness about air pollution, coupled with regulatory pushes like the National Clean Air Programme (NCAP), is prompting large and medium-scale industries to adopt VOC mitigation technologies. A growing number of industrial clusters are now including VOC concentrator systems as part of their ESG (Environmental, Social, and Governance) initiatives.

List of Key VOC’s Rotor Companies Profiled

- Seibu Giken (Japan)

- Huashijie Environment Technology (China)

- Nichias (Japan)

- Munters (Sweden)

- Taikisha (Japan)

- SATTI (Italy)

- ProFlute (Sweden)

Segment Analysis:

By Type

The market is segmented based on type into:

- Zeolite Rotors

- Activated Carbon Rotors

By Concentration Ratio

Concentration Ratio>20 Segment Leads Due to Superior Efficiency in Large-Scale Industrial Applications

The VOC’s Rotor market is segmented based on concentration ratio capabilities into:

- Concentration Ratio<10

- Concentration Ratio: 10-20

- Concentration Ratio>20

By Technology

Adsorption-Based Systems Remain Preferred for Cost-Effective VOC Recovery

The market is segmented by technology type into:

- Adsorption-based systems

- Thermal oxidation systems

- Biological treatment systems

By End-Use Industry

The market is segmented by end-use industry into:

- Oil & Gas

- Chemicals & Petrochemicals

- Pharmaceuticals

- Food & Beverage

- Automotive & Aerospace

- Electronics & Semiconductor

- Pulp & Paper

- Textile & Leather

By Application

Industrial Manufacturing Sector Dominates VOC Rotor Adoption for Emission Control

The market is segmented based on application into:

- Air Pollution Control

- Chemical & Petrochemical Industry

- Pharmaceutical & Biotechnology

- Food & Beverage Processing

- Printing & Coatings

- Semiconductor Manufacturing

- Automotive & Aerospace

- Wastewater Treatment Plants

Regional Analysis: VOC’s Rotor Market

Recent Developments and Market Trends in the VOC’s Rotor Market

- Growing Demand for VOC Control in Industrial Processes

With rising environmental regulations, industries such as chemical manufacturing, automotive, and pharmaceuticals are increasingly adopting VOC rotors for efficient emission control and air purification. - Technological Advancements in Rotor Coating Materials

Manufacturers are developing next-generation adsorption materials with enhanced durability, higher thermal stability, and better VOC removal efficiency, boosting the performance and lifespan of rotors. - Integration with Energy Recovery Systems

VOC rotor systems are now being integrated with heat recovery and energy-efficient HVAC solutions, helping reduce operational costs and lowering the carbon footprint of industrial plants. - Expansion in Asia-Pacific Markets

Rapid industrialization in countries like India, China, and South Korea is driving demand for VOC control technologies, making the region a key growth hub for rotor manufacturers and exporters. - Shift Toward Modular and Compact Designs

New VOC rotor models are designed to be compact and modular, allowing easier integration into existing facilities, especially for small and medium enterprises seeking cost-effective compliance solutions. - Government Incentives and Regulatory Push

Strengthening environmental policies such as the Clean Air Act and similar mandates in Europe and Asia are compelling industries to invest in advanced VOC abatement technologies, including rotor-based systems. - R&D in Multi-Pollutant Removal Solutions

Companies are investing in rotors capable of removing multiple pollutants (not just VOCs) by combining them with thermal oxidizers or catalytic converters, enabling comprehensive air quality management.

Download FREE Sample Report: VOC’s Rotor Market Sample

Explore Cobalt Recycling Market

About Intel Market Research

Intel Market Research delivers actionable insights in technology and infrastructure markets. Our data-driven analysis leverages:

- Real-time infrastructure monitoring

- Techno-economic feasibility studies

Competitive intelligence across 100+ countries

Trusted by Fortune 500 firms, we empower strategic decisions with precision.

International: +1(332) 2424 294 | Asia: +91 9169164321

Website: https://www.intelmarketresearch.com

Follow us on LinkedIn: https://www.linkedin.com/company/intel-market-research

The macro analyst desk brings highly sought after financial news based on market analysis, insider news and company filings.