Introduction

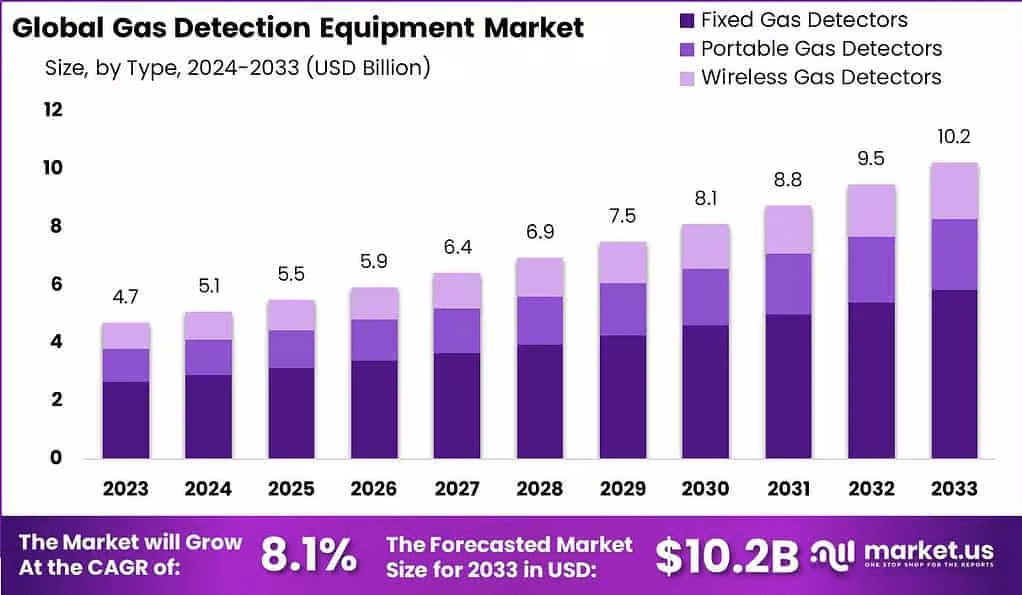

The Global Gas Detection Equipment Market, valued at USD 4.7 billion in 2023, is projected to reach USD 8.9 billion by 2033, growing at a CAGR of 6.6%, driven by stringent safety regulations and rising demand for workplace safety in industries like oil & gas, mining, and manufacturing. These devices, including fixed and portable detectors, monitor hazardous gases to prevent accidents and ensure compliance with standards like OSHA and ATEX. North America holds a 32% share, led by the U.S., while Asia-Pacific grows rapidly due to industrialization in China and India.

Key Takeaways

The market is fueled by increasing industrial accidents, with 2.3 million occupational injuries reported globally in 2023, and advancements in IoT-enabled sensors. Fixed gas detectors dominate with a 55% share, while oil & gas leads end-use applications at 28%. Challenges include high maintenance costs and false alarms, but opportunities in wireless technology and emerging markets like Asia-Pacific drive growth. North America leads, while Asia-Pacific’s rapid industrialization ensures the fastest CAGR.

Component Analysis

The market is segmented into hardware, software, and services, with hardware, including sensors and detectors, holding a 60% share in 2023 due to demand for fixed and portable gas detectors in industrial settings. Software, enabling real-time data analytics and integration with IoT platforms, is growing at a 7.2% CAGR, driven by the need for predictive maintenance and compliance reporting. Sensors with enhanced sensitivity, like electrochemical types, are critical for detecting toxic gases like CO and H2S.

Service Analysis

Services, including installation, maintenance, and calibration, account for a significant share, with maintenance services dominating in 2023 due to the need for regular sensor calibration to ensure accuracy in hazardous environments. Calibration and repair services are growing at a 6.8% CAGR, driven by regulatory compliance and the adoption of IoT for remote monitoring. Services are vital for industries like oil & gas and mining, ensuring operational safety and minimizing downtime through proactive maintenance.

Key Players Analysis

Major players like Honeywell International, MSA Safety, Drägerwerk AG, RKI Instruments, and Industrial Scientific dominate, holding over 50% of the market through advanced sensor technologies and IoT integration. Honeywell leads with its BW Technologies line, while Drägerwerk’s X-am series excels in portable detection. Recent developments include MSA Safety’s 2024 launch of ALTAIR io 4, a cloud-connected detector, and RKI’s IoT-enabled GX-3R Pro. Strategic acquisitions, like Industrial Scientific’s 2023 purchase of a sensor tech firm, enhance innovation and market reach.

Top Market Leaders

- Honeywell International Inc.

- Drägerwerk AG & Co. KGaA

- MSA Safety Incorporated

- Industrial Scientific Corporation

- RAE Systems by Honeywell

- BW Technologies by Honeywell

- Teledyne Technologies Incorporated

- Sierra Monitor Corporation

- Sensidyne, LP

- GfG Gesellschaft für Gerätebau mbH

- RKI Instruments Inc.

- Other Key Players

Conclusion

The Gas Detection Equipment Market is set for steady growth, driven by stringent safety regulations, industrial expansion, and IoT advancements. Despite challenges like high maintenance costs and false alarms, opportunities in wireless sensors and emerging markets like Asia-Pacific ensure robust expansion. North America’s dominance and key players’ focus on innovative, connected solutions position gas detection equipment as essential for workplace safety, with continued technological advancements driving the market forward through 2033.

The macro analyst desk brings highly sought after financial news based on market analysis, insider news and company filings.