The global Quantum Computing-as-a-Service (QCaaS) industry was valued at USD 2.5 billion in 2024 and is projected to reach USD 51.8 billion by 2035, growing at a remarkable CAGR of 35.8% (2025–2030). North America accounted for the largest share in 2024, driven by strong adoption in financial services, pharma, and research institutions.

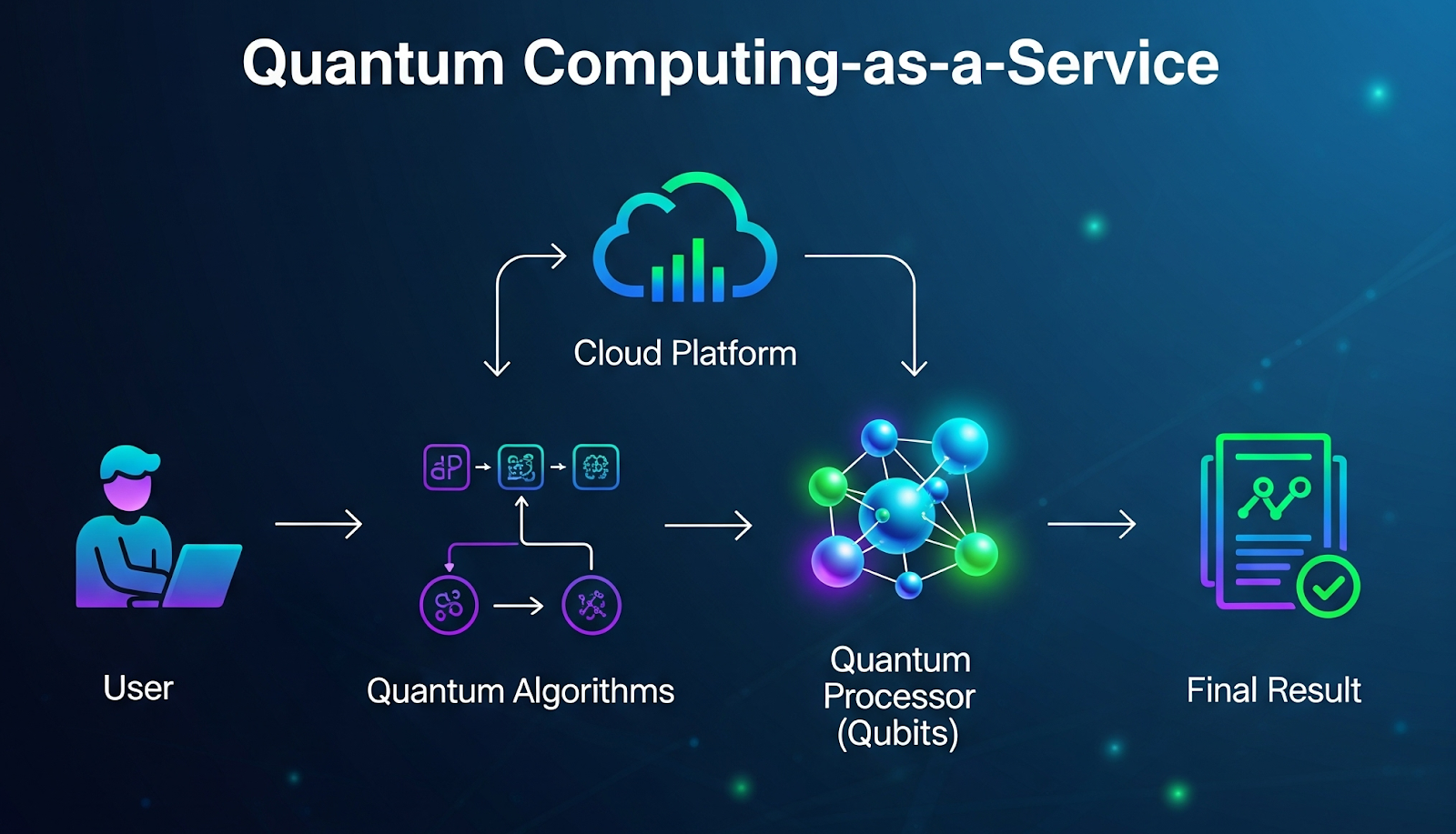

As enterprises accelerate their digital transformation, QCaaS has emerged as a scalable and cost-effective approach to leverage quantum computing power via the cloud, eliminating the need for on-premise infrastructure.

Market Overview

Quantum computing promises unprecedented computational power by leveraging the principles of superposition and entanglement. Through QCaaS platforms, businesses can access quantum resources for optimization, simulations, cryptography, and AI-driven analytics, without high capital expenditure.

Adoption is being propelled by industries such as banking & finance, life sciences, pharmaceuticals, energy, automotive, and manufacturing. The growing need for drug discovery, risk management, secure communications, and material design is fueling QCaaS investments.

Get Sample of Study Preview: https://www.prophecymarketinsights.com/market_insight/Insight/request-sample/6001

Segmentation Insights

By Service Model

- Managed QCaaS – Fully managed services, preferred by enterprises without in-house expertise.

- Self-serve QCaaS – Access for researchers and developers to run experiments directly.

- Platform as a Service (PaaS) – Development environment for building custom quantum applications.

- Others – Hybrid and emerging service offerings.

By Quantum Technology

- Superconducting – Dominant due to advancements by IBM and Google.

- Trapped-ion – Promising stability and scalability.

- Neutral Atom / Rydberg – Emerging technology for flexible architectures.

- Photonic – High potential for quantum communication and low-temperature independence.

- Spin / Semiconductor – Growing applications in integrated chip-based computing.

- Others – Hybrid approaches and experimental models.

By Deployment

- Public Cloud QCaaS – Widely accessible platforms (AWS, Microsoft Azure).

- Private / Virtual Private QCaaS – Secured access for enterprises with sensitive workloads.

- Edge / Lab Access – Specialized use cases for R&D and localized applications.

- Others – Custom deployment strategies.

By Application

- Optimization – Supply chain, logistics, and financial portfolio optimization.

- Simulation – Drug discovery, chemical modeling, and materials science.

- Cryptography & Security – Quantum key distribution, secure communications.

- Monte Carlo & Risk Analytics – Banking, trading, and insurance risk modeling.

- Research & Education – University-led and government-funded projects.

- Others – AI/ML, energy modeling, and industrial design.

By End User

- Financial Services & Insurance – Leading adoption in fraud detection, portfolio optimization.

- Life Sciences & Pharma – Breakthroughs in protein folding, clinical trials, and drug discovery.

- Chemicals & Materials – Designing advanced materials and catalysts.

- Energy & Utilities – Power grid optimization, clean energy R&D.

- Manufacturing & Automotive – Process improvement, autonomous vehicle simulations.

- Others – Defense, telecom, and government agencies.

By Region

- North America – Largest market in 2024, driven by U.S. tech giants and government funding.

- Europe – Strong quantum research initiatives in UK, Germany, France.

- Asia-Pacific – Fastest-growing region, led by China, Japan, and India.

- Latin America – Early-stage adoption in finance and energy.

- Middle East & Africa – Growing government-backed digitalization projects.

Competitive Landscape

The QCaaS industry is highly competitive and innovation-driven, with big tech companies, startups, and specialized providers all racing to commercialize quantum services.

Key Companies Profiled:

- Amazon Web Services, Inc. – Braket service for QCaaS with broad ecosystem support.

- Microsoft – Azure Quantum platform integrating multiple hardware partners.

- IBM – Pioneer with IBM Quantum Experience and large quantum processor roadmap.

- D-Wave Quantum Inc. – Leader in quantum annealing solutions.

- Xanadu – Photonic quantum computing provider with open-source toolkits.

- Oxford Quantum Circuits (OQC) – UK-based firm focusing on scalable superconducting qubits.

- BlueQubit – Innovative startup offering developer-friendly platforms.

- Honeywell International Inc. – Industrial leader leveraging trapped-ion technology.

- PsiQuantum – Building scalable photonic quantum computers.

- Atos SE – Quantum simulators and hybrid solutions.

- PASQAL – France-based neutral atom computing specialist.

- Qilimanjaro Quantum Tech – Hybrid quantum-classical solutions.

- Riverlane – Quantum operating system developer.

- QC Ware – Enterprise-focused software provider.

- Multiverse Computing – Quantum algorithms for financial applications.

Growth Drivers

- Cloud-based Accessibility – Democratization of quantum computing without infrastructure costs.

- AI & Machine Learning Integration – QCaaS enhancing deep learning, pattern recognition, and big data analytics.

- Government & Defense Investments – Strategic funding in the U.S., EU, and Asia-Pacific.

- Pharmaceutical Research – Quantum simulations accelerating drug discovery and vaccine development.

- Data Security Needs – Quantum cryptography addressing post-quantum cybersecurity challenges.

Recent Developments

- IBM announced a 1000+ qubit processor roadmap by 2026 to power enterprise-grade QCaaS.

- Microsoft expanded Azure Quantum partnerships with Honeywell and Rigetti in 2024.

- AWS launched new optimization-focused Braket services for supply chain management.

- D-Wave signed deals with Japanese firms to explore manufacturing simulations.

- PsiQuantum secured major funding for its scalable photonic quantum platform.

Strategic Insights

- Partnerships between tech giants and startups are accelerating commercialization.

- Hybrid quantum-classical computing models are bridging the current performance gap.

- Enterprises should explore pilot projects in finance, pharma, and logistics to build early competitive advantage.

- Talent acquisition and training in quantum software development remains a priority for scaling adoption.

Business Relevance

For startups and investors, QCaaS represents one of the fastest-growing tech sectors globally. With applications spanning finance, energy, healthcare, automotive, and cybersecurity, the opportunity for disruptive business models is immense. Early movers can leverage partnerships, niche applications, and regional collaborations to gain a foothold.

Frequently Asked Questions (FAQs)

Q1. What is the current size of the QCaaS industry?

In 2024, the QCaaS industry was valued at USD 2.5 billion.

Q2. What will be the market size by 2035?

The industry is projected to reach USD 51.8 billion by 2035.

Q3. What is the CAGR during 2025–2030?

The QCaaS market is expected to grow at a CAGR of 35.8%.

Q4. Which region dominates the market?

North America was the largest regional market in 2024.

Q5. Who are the leading players?

IBM, AWS, Microsoft, D-Wave, Honeywell, PsiQuantum, and Xanadu are among the key players.

Author: Shweta R., Business Development Specialist at Prophecy Market Insights

The macro analyst desk brings highly sought after financial news based on market analysis, insider news and company filings.