Introduction:

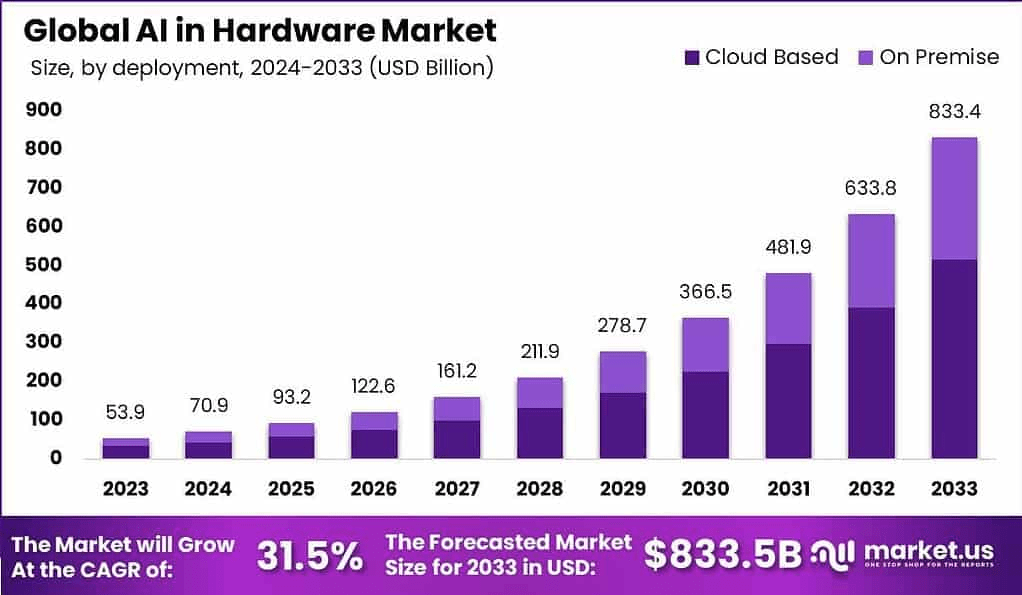

The AI in Hardware Market is projected to exceed USD 90 billion by 2030, growing at a CAGR of 25.3% from 2024. This growth is fueled by the rising demand for high-performance computing in AI applications across data centers, autonomous vehicles, robotics, healthcare, and edge devices. Specialized AI chips like GPUs, TPUs, and neuromorphic processors are replacing traditional CPUs for their efficiency in handling AI workloads. Increasing deployment of AI-powered devices and the evolution of real-time inference tasks in sectors like manufacturing and finance are driving the demand for powerful, energy-efficient, and scalable hardware solutions globally.

Key Takeaways:

- Market to exceed USD 90 billion by 2030

- CAGR of 25.3% driven by AI-centric applications

- Rising need for AI chips in edge and data centers

- GPUs and ASICs dominate for deep learning workloads

- AI hardware critical for real-time inference in robotics

- Growth in autonomous systems fuels chip innovation

- Energy-efficient AI processors gain traction

- Demand from healthcare, automotive, and IoT industries

- Integration with cloud and edge networks expanding

- Asia-Pacific leads in hardware production and deployment

Emerging Trends:

Neuromorphic computing is gaining traction for ultra-low power AI tasks. Edge AI hardware is expanding with SoCs that integrate AI accelerators for local inference. Quantum processors are being researched to enhance complex AI calculations. Heterogeneous architectures, combining CPUs, GPUs, and NPUs, are becoming mainstream. Open-source hardware initiatives are supporting customizable AI chip designs. 3D chip stacking and chiplet integration enhance processing density. AI workloads are being increasingly handled on FPGA-based hardware for flexibility. TinyML is enabling microcontroller-based AI for embedded systems. Hardware-software co-optimization is accelerating, ensuring AI models align with specific silicon capabilities. Sustainability-focused AI hardware is on the rise.

Use Cases:

- Real-time decision-making in autonomous vehicles

- AI-driven image and speech recognition on mobile devices

- Industrial automation using edge-based inference chips

- Healthcare diagnostics and medical imaging acceleration

- AI-powered surveillance with on-device analytics

- Natural language processing in voice assistants

- Smart agriculture with AI-driven sensor platforms

- Predictive maintenance in manufacturing via IoT + AI chips

- Augmented reality and gaming with enhanced AI graphics chips

- High-speed trading and risk analysis in financial systems

Major Challenges:

Designing AI-specific hardware that balances performance, cost, and energy use is complex. Heat dissipation and power consumption remain major barriers for high-performance chips. Hardware obsolescence is rapid due to fast-evolving AI models. Lack of standardization hampers interoperability across platforms. Ensuring compatibility between AI software and new hardware architectures is challenging. Development costs and long time-to-market hinder smaller players. Global chip shortages and supply chain disruptions affect delivery. Security vulnerabilities in hardware-level AI execution pose risks. Limited availability of skilled talent for AI chip design impacts innovation. Ethical concerns arise around surveillance hardware and military-grade AI deployments.

Opportunities:

Edge computing growth drives demand for compact, efficient AI chips. Increasing use of AI in healthcare and defense opens high-value verticals. Investment in AI R&D from governments and tech giants fosters innovation. Emerging markets offer new demand for affordable AI hardware. Integration of AI in consumer electronics, from TVs to wearables, expands addressable market. Demand for AI in cloud data centers drives custom ASIC and FPGA design. Collaboration with universities boosts academic-industry breakthroughs in processor design. AI hardware tailored for sustainability and carbon-efficient computing gains investor interest. Expansion of smart cities fuels public infrastructure-based AI deployments. Software-hardware integration services offer recurring revenue streams.

Key Players Analysis:

The AI in Hardware Market consists of global semiconductor manufacturers, niche AI chip designers, and cloud infrastructure providers developing in-house silicon. Players compete based on chip architecture, processing power, energy efficiency, and adaptability to evolving AI models. Leaders invest in R&D for advanced fabrication nodes, chiplet integration, and quantum experimentation. Partnerships with hyperscalers, automakers, and robotics firms extend market reach. Open hardware ecosystems and software toolchain support are differentiators. Competitive advantage lies in balancing cost, performance, and scalability across data center, edge, and consumer applications. Market players focus on secure, ethical, and high-throughput AI execution at device and network levels.

Conclusion:

The AI in Hardware Market is a cornerstone of the broader AI ecosystem, enabling rapid, efficient, and scalable intelligence across industries. As AI applications become increasingly sophisticated and widespread, the demand for specialized, high-performance hardware grows in parallel. Despite technical and supply chain challenges, the market benefits from relentless innovation in chip architecture, edge computing, and real-time processing capabilities. With AI becoming integral to modern infrastructure—from cars to cloud—the future belongs to hardware solutions that can adapt to the evolving landscape of intelligent computing. The sector is set for long-term expansion, driven by both technological necessity and strategic investment.

The macro analyst desk brings highly sought after financial news based on market analysis, insider news and company filings.