Introduction:

The Aviation Cloud Market is projected to exceed USD 12.4 billion by 2030, growing at a CAGR of 16.5% from 2024. With airlines and airports embracing digital transformation, cloud-based technologies are being adopted to enhance operational efficiency, scalability, data analytics, and passenger experience. Cloud computing in aviation supports real-time flight tracking, predictive maintenance, and dynamic resource planning. Growing demand for cost-effective infrastructure, increased air traffic, and the need for resilient IT systems post-pandemic are fueling market expansion. Cloud platforms also enable seamless integration of AI, IoT, and cybersecurity for end-to-end aviation management and automation.

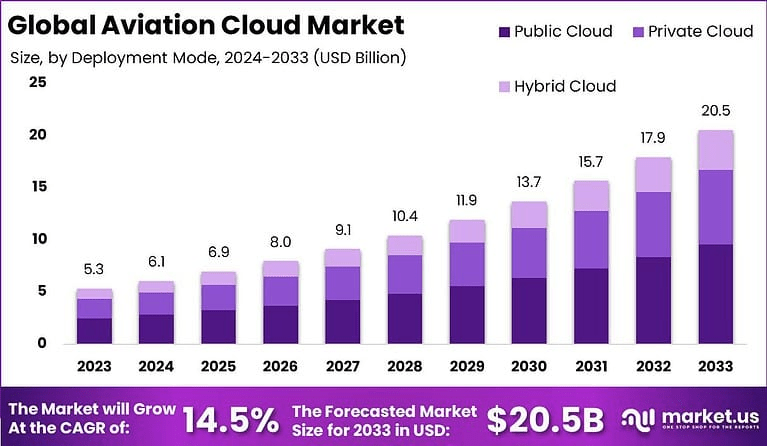

Key Takeaways:

- Market to surpass USD 12.4 billion by 2030

- CAGR of 16.5% driven by demand for digital efficiency

- Real-time analytics optimize flight operations

- Cloud enables scalable and cost-efficient IT infrastructure

- Adoption rising in airports, airlines, and MRO providers

- Key use in predictive maintenance and resource planning

- Growth spurred by AI and IoT integration

- Enhances passenger engagement and safety

- Cloud-based cybersecurity strengthens data protection

- Strong demand for SaaS and hybrid cloud solutions

Emerging Trends:

Adoption of hybrid and multi-cloud strategies is growing to ensure flexibility and data sovereignty. AI-driven predictive maintenance powered by cloud analytics is reducing aircraft downtime. Blockchain on cloud platforms is being tested for secure parts traceability and passenger ID management. Digital twins of aircraft systems are emerging through cloud-hosted IoT data. Integration of AR/VR training modules via the cloud improves pilot and ground staff training. Cloud-based crew and flight scheduling tools are automating airline operations. Enhanced cybersecurity protocols on cloud networks protect sensitive aviation data. Cloud-native mobile applications enhance in-flight services. Demand for private cloud deployments is increasing among defense and national carriers.

Use Cases:

- Real-time flight tracking and performance monitoring

- Cloud-hosted predictive maintenance for fleet efficiency

- Passenger service systems (check-in, boarding, feedback)

- Digital crew management and rostering solutions

- Aircraft health monitoring through IoT-cloud integration

- Dynamic pricing and revenue management engines

- Air traffic and ground handling optimization

- Secure document management for compliance and audits

- Disaster recovery and business continuity planning

- Cloud-based cybersecurity frameworks for airline IT systems

Major Challenges:

Data privacy concerns, particularly in international cloud operations, pose regulatory hurdles. Integration with legacy systems delays cloud adoption. High costs of transition, especially for smaller carriers, remain a barrier. Ensuring uninterrupted connectivity in aviation environments is technically complex. Cybersecurity risks from centralized cloud data require strong mitigation. Lack of skilled personnel to manage and migrate to cloud platforms hampers implementation. Vendor lock-in concerns affect long-term planning. Differing global regulations create compliance complexities. Limited standardization across cloud aviation platforms reduces interoperability. Downtime in cloud services can disrupt critical flight operations.

Opportunities:

Rising air traffic and digital passenger expectations create demand for scalable cloud systems. Green aviation initiatives align with efficient, energy-saving cloud IT models. Increased adoption of SaaS platforms supports MRO, logistics, and flight operations. Expansion in emerging markets fuels demand for cost-effective IT via cloud. Government investments in smart airports create cloud infrastructure opportunities. Advanced analytics in fuel management and crew planning offer ROI potential. The shift to remote operations and e-learning boosts demand for cloud-based training platforms. Disaster recovery solutions are in high demand post-COVID. Growing interest in edge computing enhances real-time decision-making. Collaboration with tech providers enables innovation in aviation IT ecosystems.

Key Players Analysis:

The Aviation Cloud Market comprises cloud computing giants, aviation IT providers, and specialized SaaS vendors. These players offer tailored solutions for airline operations, airport management, MRO systems, and passenger engagement. Competitive strengths include scalability, integration with legacy aviation systems, regulatory compliance, and real-time analytics. Firms are enhancing product offerings with AI, blockchain, and cybersecurity tools. Many invest in hybrid cloud environments for flexibility and resilience. Differentiators include vertical specialization, global service delivery capabilities, and uptime reliability. Strategic alliances with OEMs, airlines, and airport authorities are common. Continuous innovation, customer support, and adherence to aviation safety standards shape vendor positioning.

Conclusion:

The Aviation Cloud Market is poised for sustained growth as the industry modernizes for efficiency, safety, and passenger satisfaction. With the proliferation of digital aircraft systems and rising operational complexity, cloud technologies offer the agility and intelligence aviation stakeholders need. Though challenges around security, integration, and regulation persist, the benefits of scalability, cost reduction, and real-time analytics are compelling. As cloud platforms evolve to incorporate AI, IoT, and cybersecurity, they will become central to the aviation ecosystem. The market offers expansive opportunities for vendors and operators ready to embrace the next generation of aviation IT infrastructure.

The macro analyst desk brings highly sought after financial news based on market analysis, insider news and company filings.