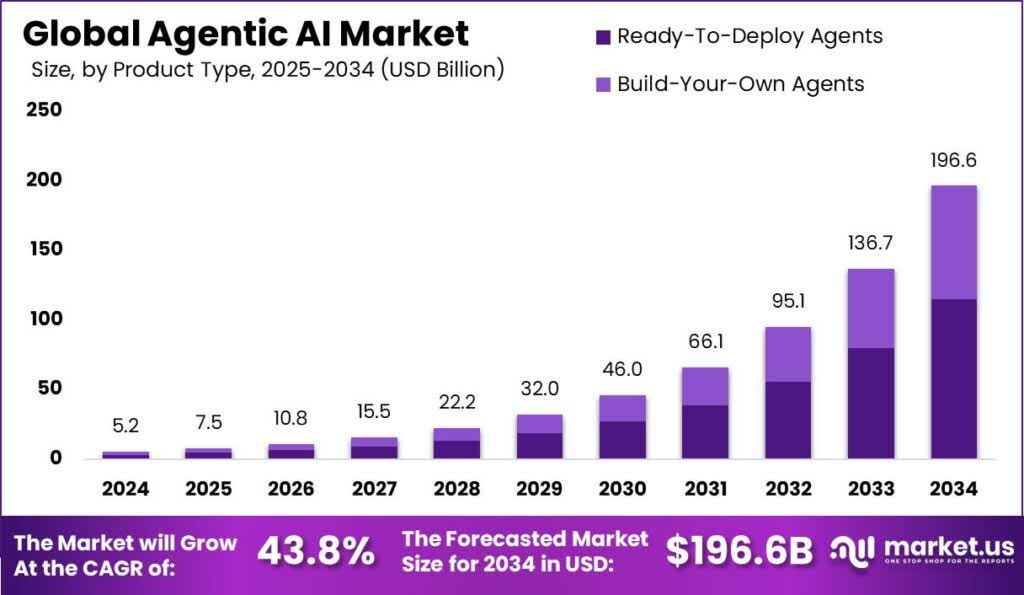

The global Agentic AI market is entering a transformative decade, marked by unprecedented growth and technological advancement. As of 2024, the market has been valued at approximately USD 5.2 billion, with projections indicating it will reach nearly USD 196.6 billion by 2034, expanding at an impressive CAGR of 43.8%. This extraordinary rise is being driven by the increasing integration of AI systems capable of autonomous decision-making, task execution, and adaptive behavior across industries such as finance, healthcare, manufacturing, and defense. The shift toward AI agents that operate with goal-oriented intelligence is setting a new benchmark for intelligent automation in enterprise ecosystems.

The adoption of agentic AI is accelerating at a remarkable pace, fundamentally reshaping enterprise software and operational landscapes. As reported by DigitalDefynd, by 2028, an estimated 33% of enterprise software applications will embed agentic AI capabilities, a dramatic leap from under 1% in 2024. This evolution is expected to enhance operational efficiency by 30% and reduce processing times by up to 40%, particularly in complex, data-intensive sectors like manufacturing and logistics. The growing demand reflects a broader industry shift toward intelligent automation that not only streamlines workflows but also drives real-time decision-making and autonomous execution.

From a market positioning perspective, 90% of businesses foresee agentic AI as a critical determinant of competitive advantage within the next five years. This sentiment is reinforced by Deloitte’s findings, where organizations leveraging AI in strategic functions reported 15% higher market share and demonstrated superior performance in both revenue generation and innovation delivery. The capability of agentic systems to learn, act independently, and continuously optimize is now being viewed as essential to maintaining leadership in dynamic digital markets.

The healthcare industry is also poised for transformational benefits. According to Accenture, the implementation of agentic AI could result in annual cost savings of approximately USD 50 billion, driven by increased efficiencies in drug discovery, diagnostics, and personalized treatment pathways. The American Hospital Association further highlights that AI has already helped reduce diagnostic errors by 20% and treatment costs by 15%, signaling strong proof-of-concept and encouraging broader adoption across health networks.

On the consumer front, the shift toward AI-powered personalization is becoming increasingly influential. A HubSpot survey revealed that 75% of consumers prefer interacting with brands offering AI-enhanced personalization, which has been linked to a 40% increase in customer retention. Moreover, as ethical considerations grow in prominence, findings from Harvard Business Review emphasize that companies adhering to responsible AI frameworks witness 20% higher trust levels from their users. This underscores that trust, transparency, and user-centric design will be foundational pillars in the successful deployment of agentic AI at scale.

Key Insight Summary

- In 2024, the Ready-To-Deploy Agents segment led the market with a 58.5% share, as businesses increasingly favored pre-built, customizable AI agents to accelerate adoption and reduce development time.

- The Productivity & Personal Assistant application dominated with a 28.2% share in 2024, reflecting growing demand for AI agents that enhance individual and workforce efficiency through task automation and smart scheduling.

- The Multi Agent architecture held a commanding 66.4% share, highlighting a preference for collaborative agent ecosystems capable of handling complex, distributed workflows with minimal human oversight.

- By end-user, Enterprises captured over 62.7% of the market, driven by large organizations adopting agentic AI to streamline operations, cut costs, and deliver more personalized customer engagement.

- The U.S. market was valued at USD 1.58 billion in 2024, with a robust projected CAGR of 43.6%, fueled by technological maturity, strong venture capital backing, and a culture of early enterprise adoption.

- North America as a whole led globally, holding a 38% market share in 2023, underscoring its leadership in AI research, deployment, and policy alignment.

- According to Financial Express, 33% of enterprise applications are expected to feature Agentic AI by 2028, a steep increase from under 1% in 2024, signaling rapid mainstreaming of autonomous digital agents.

- OECD findings reveal that 90% of constituents are already prepared to engage with AI agents in public service delivery, pointing to strong societal readiness and acceptance for agent-driven governance.

Regional Analysis

In terms of regional leadership, North America maintained a clear edge in 2024, accounting for over 38% of the global market, which translated to around USD 1.97 billion in revenue. This dominance is largely fueled by the region’s strong technological infrastructure, robust venture capital investment, and early-stage adoption of AI-driven agents in both commercial and federal sectors.

The United States, in particular, has shown remarkable momentum, registering a market size of USD 1.58 billion in 2024 alone, supported by growing demand for autonomous digital agents in cybersecurity, customer experience, and operational optimization. With a CAGR of 43.6%, the U.S. market is expected to remain a pivotal force in shaping global Agentic AI developments over the next decade.

Emerging Trend: Hyperautomation with Decision Intelligence

Agentic AI is increasingly driving hyperautomation, evolving beyond simple task automation to full-cycle, adaptive workflows. Systems can now analyze real-time data, choose optimal steps, and reroute actions as needed – extending autonomy into strategic decision-making and dynamic planning.

This trend has been particularly noted in sectors such as IT operations and service delivery, where agentic systems can monitor conditions, make real-time decisions, and execute corrective steps without human intervention. These developments emphasize efficiency gains and operational agility superior to rule-based automation frameworks.

Driver: Integrating Tool Use and Long-Term Memory

The rise of agentic AI is supported by advances in tool integration and contextual memory frameworks. Modern architectures allow agents not only to access APIs and operate databases but to retain long-term context, enabling decision continuity across sessions .

This driver enhances capability: agents become reliable over repeated interactions, learning preferences and system states. Agents now operate proactively, coordinating multistep tasks and offering seamless escalation or collaboration support – marking a shift from reactive to anticipatory AI.

Restraint: Privacy, Security, and Cyber Risks

The deployment of agentic agents raises data protection and cybersecurity concerns. These systems often require extensive access to sensitive internal or customer data, making them prime targets for breaches or malicious exploitation.

Cybersecurity experts warn that increased connectivity – even across secure environments – amplifies attack surfaces. Inadequate oversight or vulnerability in agentic systems may result in unauthorized data access, unintended action, or regulatory penalties, thereby restraining widespread adoption.

Opportunity: Domain‑Specific Small AI Models

Emerging research suggests that small, specialized language models (SLMs) may outperform large generalist AI when embedded in agentic systems. SLMs reduce cost and resource overhead while delivering dependable performance within narrow domains.

Applying SLMs in focused tasks – such as financial processing, IT operations, or customer scripting – offers measurable ROI. Organizations can gain precision control and efficiency, while minimizing complexity, prompting wider adoption in enterprise contexts sensitive to resource costs and reliability requirements.

Challenge: Accountability and Ethical Oversight

The autonomous nature of agentic agents introduces complex accountability and liability challenges. When decisions lead to unintended or harmful outcomes, legal responsibility becomes unclear due to dispersed agency across models, developers, operators, and stakeholders.

This “moral crumple zone” creates risk for organizations deploying agents in high-stakes contexts. Failure to embed robust oversight frameworks – including audit trails, ethical governance, and legal clarity – can undermine trust and trigger regulatory or reputational consequences, slowing adoption.

Key Market Segments

By Product Type

- Ready-To-Deploy Agents

- Build-Your-Own Agents

By Agent Role

- Customer Service and Virtual Assistants

- Sales and Marketing

- Human Resources

- Legal and Compliance

- Financial Services

- Other Applications

By Agent System

- Single Agent

- Multi Agent

By End User

- Enterprises

- BFSI

- IT & Telecom

- Government & Public Sector

- Healthcare

- Manufacturing

- Media & Entertainment

- Others

- Consumers

Top Key Players in the Market

- Amazon.com Inc.

- Alphabet Inc.

- Microsoft Corporation

- IBM Corporation

- Oracle Corporation

- Salesforce, Inc.

- SAP SE

- ServiceNow, Inc.

- UiPath, Inc.

- Zendesk, Inc.

- Others

Discover More @ https://market.us/report/agentic-ai-market/

The macro analyst desk brings highly sought after financial news based on market analysis, insider news and company filings.