Introduction

The Electrostatic Discharge (ESD) Protection Devices Market plays a vital role in safeguarding sensitive electronic components from damage caused by sudden electrostatic surges. As electronic systems become smaller, faster, and more complex, the need for robust ESD protection grows exponentially—especially in sectors such as consumer electronics, automotive, industrial automation, and telecommunications. These devices are integrated into circuit designs to ensure long-term reliability, reduce failure rates, and comply with safety and durability standards. The expanding use of connected devices and IoT ecosystems has made ESD protection an essential part of modern electronics design.

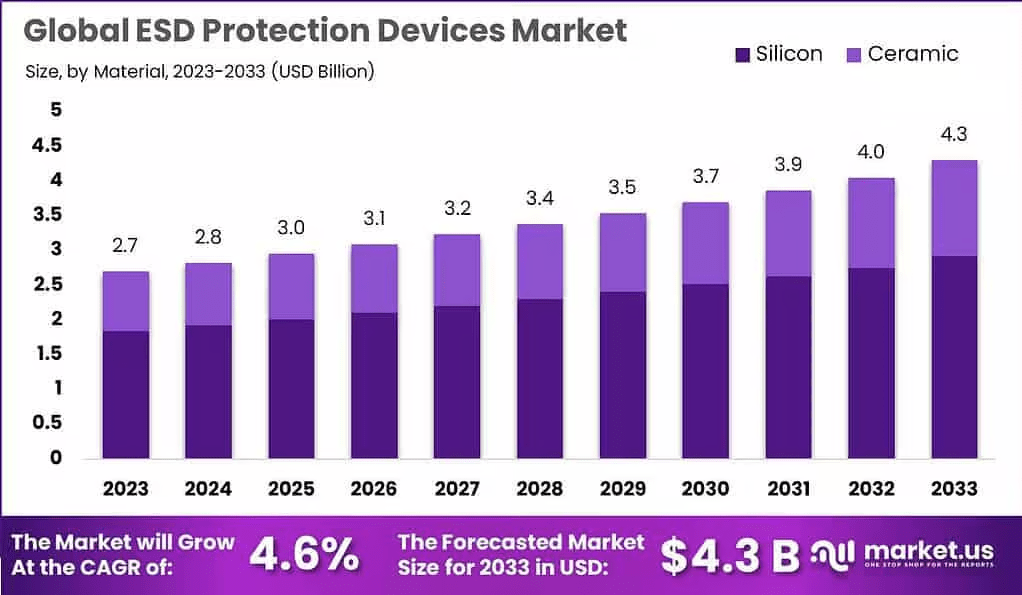

Key Takeaways

The ESD protection devices market is witnessing strong growth due to increasing demand for miniaturized and high-speed electronic components that are more vulnerable to ESD damage. Rising adoption of smartphones, wearables, automotive electronics, and 5G-enabled devices is driving the need for compact and efficient ESD solutions. Trends include the shift toward silicon-based and polymer-based protection technologies, the integration of ESD components into multi-function ICs, and rising demand for devices compliant with international electrostatic standards. Asia-Pacific dominates the market, driven by large-scale electronics manufacturing, with North America and Europe following closely behind.

Component Analysis

Key components in the ESD protection ecosystem include diodes (TVS diodes, Zener diodes), metal oxide varistors (MOVs), polymer-based ESD suppressors, and on-chip ESD protection circuits. TVS (Transient Voltage Suppression) diodes are among the most commonly used components due to their fast response and compact size. MOVs are typically used in industrial and AC power applications. Polymer ESD suppressors offer flexible design options and are well-suited for mobile devices. On-chip ESD protection is increasingly being integrated into semiconductor designs to protect internal circuitry, reducing the need for discrete components in compact designs.

Service Analysis

Services in the ESD protection market include custom protection solution design, failure analysis and testing, regulatory compliance consulting, and product integration and prototyping. Manufacturers and engineering service providers assist clients with selecting and integrating ESD components based on application-specific voltage, capacitance, and current handling needs. Testing services ensure that protection devices meet IEC and JEDEC standards. Additionally, technical consulting services help OEMs align with EMI/ESD regulations and improve product lifecycle reliability. These services are especially crucial in automotive, aerospace, and medical electronics, where system integrity is critical.

Key Player Analysis

Leading players in the ESD protection devices market include Texas Instruments, Infineon Technologies, Nexperia, STMicroelectronics, ON Semiconductor, Littelfuse, Murata Manufacturing, and Vishay Intertechnology. These companies offer a wide range of discrete and integrated ESD protection solutions tailored to different voltage levels, form factors, and response times. Texas Instruments and STMicroelectronics are known for their innovations in automotive-grade and industrial ESD components. Littelfuse and Murata dominate the market in polymer and surface-mount ESD protection devices. Players are focusing on miniaturization, higher bandwidth compatibility, and integration with system-level protection architectures to stay competitive.

Top Market Leaders

- Murata Manufacturing

- STMicroelectronics

- Texas Instruments Inc.

- Nexperia

- Littlefuse Inc.

- Bourns Inc.

- Semtech Corporation

- ROHM Semiconductor

- ProTek Devices

- Infineon Technologies

Conclusion

As electronic devices become increasingly interconnected and compact, the need for reliable and efficient ESD protection has never been more critical. The ESD Protection Devices Market will continue to grow as industries push for higher performance and durability in their products. Innovations in materials, form factor reduction, and integration will shape the next phase of this essential segment in the electronics supply chain.

The macro analyst desk brings highly sought after financial news based on market analysis, insider news and company filings.